Can farms really outperform their neighbors?

According to a study from the University of Illinois, the answers is yes.

To view the study, click here: http://farmdocdaily.illinois.edu/2017/05/how-hard-is-it-to-be-above-average-in-farming.html. They studied whether or not a farmer can truly outperform their peers assuming similar variables (location, soil type, off-farm income level, etc). Returns obviously vary from year-to-year but certain farms have shown an ability to consistently outperform their peers.

See below for a summary of the study.

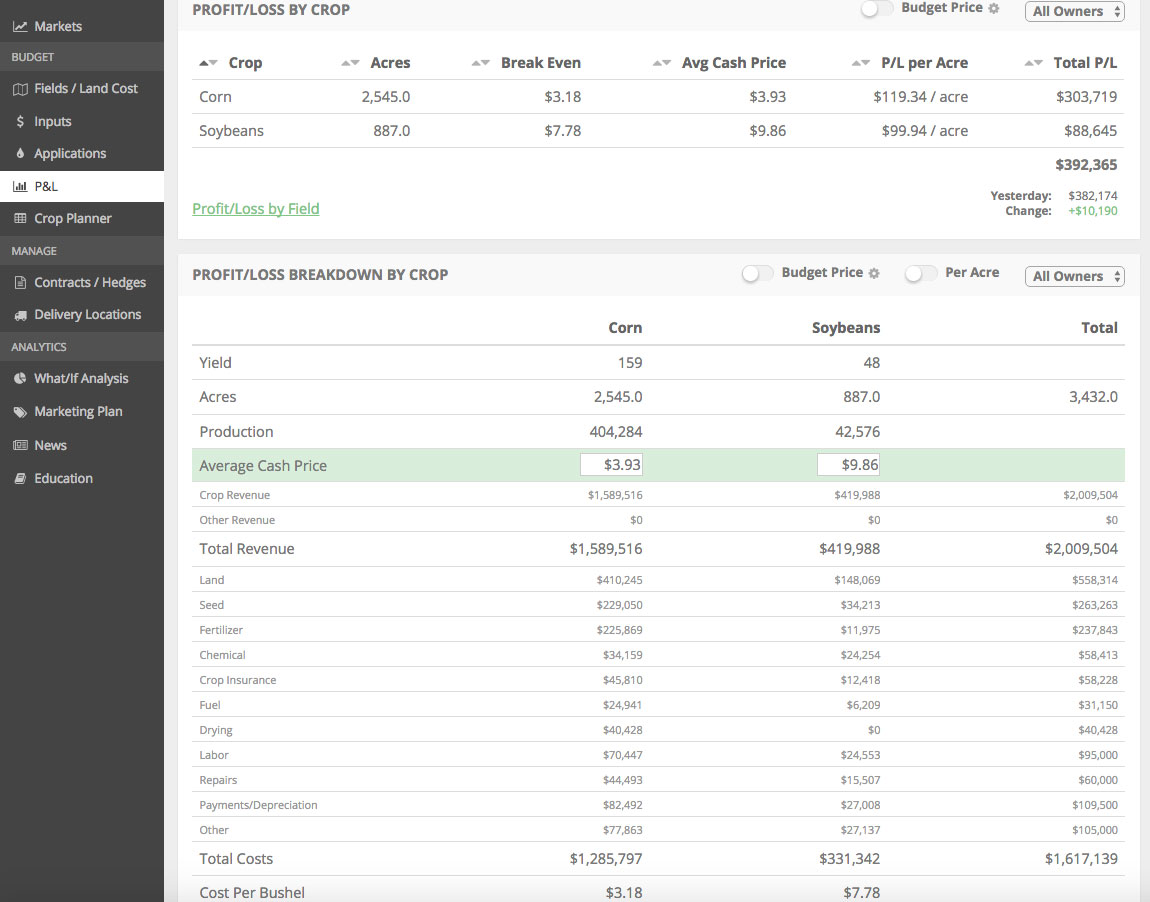

“Returns to farms vary from one year to next due to variation in prices, yields, and costs. Within a year, some farms will have higher returns than others. Over time, there are some farms that tend to persist in having high returns. Over time, the returns of these more profitable farms tend to average $20 and $30 per acre higher than the average of all farms.”

Even I was surprised that the gap was that high. $20-30/acre…..wow!

What can you do to increase your farm’s likelihood of outperformance? While I could talk about this forever, here’s a list of a few things which I feel give farmers a financial advantage. Many of these aren’t new and they aren’t rocket science.

- Producing above average cost-adjusted yields in your area. You need to constantly and proactively seek ways to increase ROI in your agronomic decisions. Common sense, I know, but still very important.

- The ability to say no. Saying no to impulse (or tax-motivated) equipment purchases, snake oil salesman, and high land cost decisions (rent & purchase) are just a few of many the ways that doing nothing oftentimes gives your farm a profitability advantage.

- Being OK with the market moving higher after a sale or hedge. Rallies can punish those that are proactive. Remember that past decisions are sunk costs that can’t be changed. Do what’s best for your farm today!

- Using your grain storage like an elevator. Grain storage can provide some of the highest ROI opportunities on a farm. See this blog post for more on this topic: An Example of a Great Grain Storage ROI

- Understand biases. Everyone you work with has a bias. Your agronomist wants you to maximize yield. Your local grain merchandiser would love to have your grain. Your banker would love to have you generate the bank more interest with the same or less risk. We would like you to use our software. Most of the time this group of people is looking out for your best interest, but not always! You are the boss so look out for your business’ interests first.

- Have a thirst for knowledge. You never know when/where you’re going to learn something that will allow you to add dollars to the bottom line. Speaking of this, we’re going to open our Business of Farming online course again soon. Keep your eye open for it.

- Understand that farming is loaded with uncertainty, from both a market and weather standpoint. Accept that as fact and try to be comfortable making proactive decisions even though you can’t know for certain how each of those factors will impact your decision.

They key with all of these is being comfortable with an active (proactive) vs. a passive (reactive) decision-making process.

Your past decisions are crystal clear with the benefit of hindsight. When your proactive decision turns out to not be “correct”, don’t beat your self up over it. Put the proabilities on your side and don’t judge your decision solely with the benefit of hindsight.

Click here to view a blog post we wrote on how statistics should drive your farm management decisions.

All-in-all, an investment (time or money) in your farm’s management can pay big dividends over time.

If you enjoyed this post, look below for a handful of additional posts we’ve written over the last couple years.

Nick Horob

Passionate about farm finances, software, and assets that produce cash flow (oil wells/farmland/rentals). U of MN grad.

Related Posts

8 Ways to Increase Farm Profitability in 2017

In this blog post, we discuss actionable ideas to help you increase the profitability of your farm in 2017. In reviewing the financials of 100's farms, we've seen these farm management best practices yield strong long-term results.

Read More »I Recently Met a Farmer in His 50's That Owns 3,000 Acres Free and Clear

In this blog post, we discuss a recent meeting we had with a farmer who owns 3,000 acres of debt-free farmland. We walk through the strategies this farmers has utilized to build a sizable net worth in a volatile farming environment.

Read More »Grain Marketing can be an Emotional Roller Coaster

Grain marketing is hard! Volatile commodity markets lead to frustration, greed, and indecision. Today's farmer needs to work hard to find a risk management system that allows them to make less emotional, and more profitable, grain marketing decisions.

Read More »